Supply Chain Finance vs. Financing-Based Trade: The Fine Line That Defines Credibility and Collapse

A Blurred Line with Billions at Stake

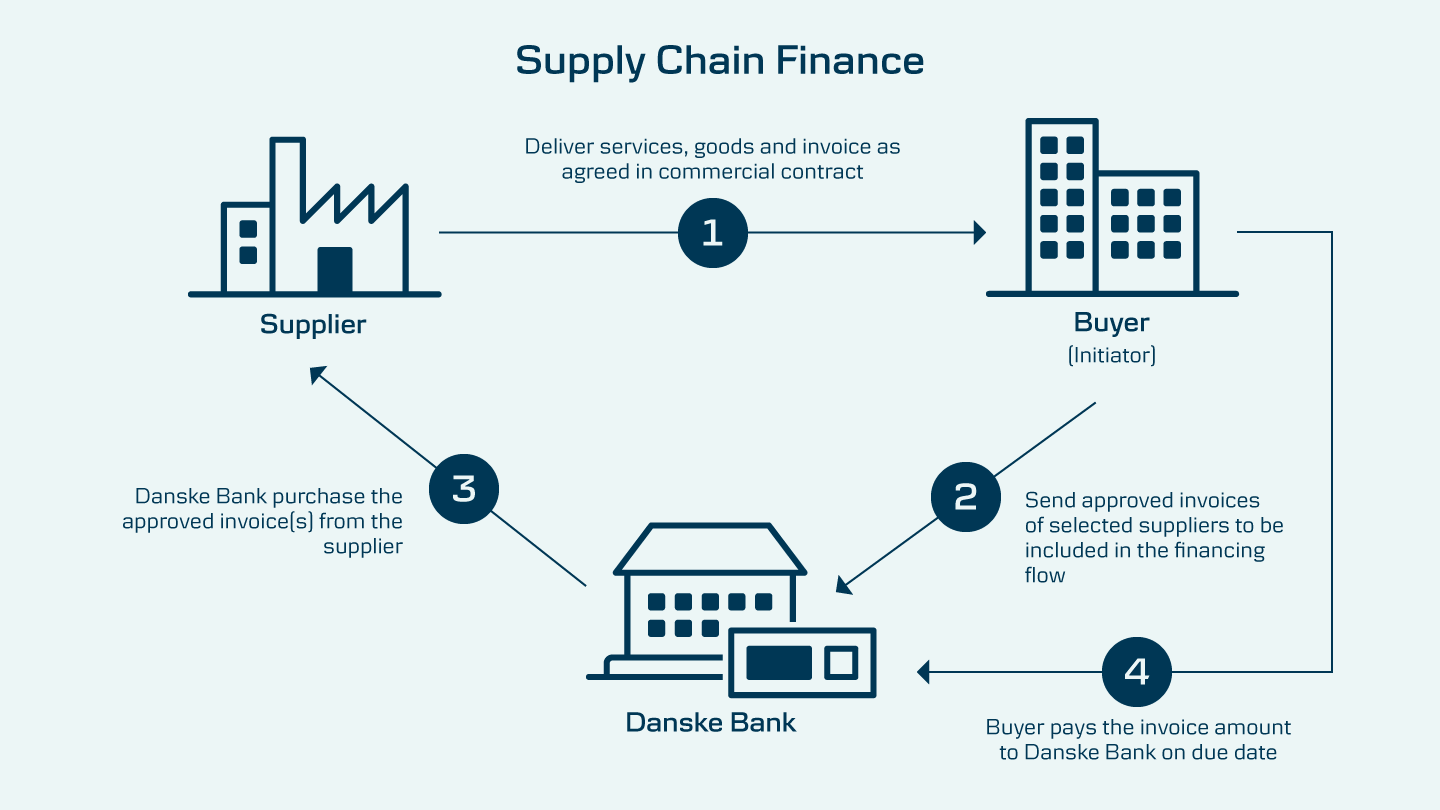

In the high-stakes world of global trade and liquidity management, a subtle but consequential distinction is redefining the financial supply chain: **real supply chain finance ** versus financing-based trade. Though the two are often conflated, their differences mark the line between legitimate financial services and precarious pseudo-banking models that have toppled billion-dollar firms.

As the global economy leans harder into integrated logistics, inventory-as-a-service, and working capital optimization, understanding this dichotomy has become essential for every serious investor, trade operator, and banker. And nowhere is this more apparent than in the cold, steel-lined corridors of industrial storage facilities—like one run by a private company that claims to operate the largest cold storage facility in its region, housing over 10,000 tons of temperature-controlled inventory. This infrastructure is not just about frozen seafood or seasonal produce; it's about trust, collateral, and the new frontier of asset-based finance.

When Iceboxes Become Banks: A Real-World SCF Example

At first glance, the business might appear mundane—storage, logistics, service bundling. But beneath the surface lies a fully functioning financial engine. When a seafood distributor arrives with $200,000 in hand to purchase $400,000 worth of inventory, the warehouse operator facilitates a loan for the remaining $200,000. How? Through a symbiotic partnership involving banks and third-party guarantors.

"The distributor stores all $400,000 worth of frozen seafood in our warehouse as collateral," one executive explained. "We coordinate a guarantee and facilitate inventory tracking and liquidation rights in case of default."

Here, the storage provider does not take on trading risk. It does not purchase or sell goods. Instead, it orchestrates the financial mechanics—securing a 3–4% loan from a bank, adding a 1.5% guarantee fee, and baking in a 6% service premium under the guise of storage fees. The result is a total cost to the distributor of approximately 12% annually. Importantly, these services are not optional. Clients must use integrated offerings—storage, logistics, financing—all bundled under one operational ecosystem.

This, insiders argue, is true supply chain finance. It’s asset-backed, bank-integrated, and risk-managed—an infrastructure-first model that prioritizes service and credit intermediation, not speculative trading.

The Mirage of Financing-Based Trade

Contrast this with the growing crowd of operators engaging in what’s misbranded as SCF but is functionally just financing-based trade.

These entities insert themselves as buyers and sellers—purchasing goods from suppliers and flipping them to end-users while structuring their margins as disguised interest. The contractual paperwork might resemble a financing deal, but the economic reality is unmistakably trading. Some tolerate this model for its higher yields (15–20% annually), but the foundations are brittle.

"People think they're doing finance, but it's just risk-wrapped trade," one analyst remarked. "When defaults hit, there's no infrastructure to backstop losses, no real collateral control—just paper and promises."

Banks, meanwhile, are getting wise. Where once $100 million in trade flows could fetch $20 million in credit lines, financial institutions are now asking deeper questions. With regulatory bodies circling and post-Greensill caution prevailing, funding appetites have cooled—especially for businesses without tangible infrastructure or real operational skin in the game.

Sector Deep Dive: Real-World SCF in Action

🧺 Agricultural Supply Chains

Seasonal cash cycles make farming a prime candidate for SCF. Cooperative groups can collateralize harvests stored in centralized silos, with banks lending pre-harvest funds against insured, trackable produce. This setup improves reinvestment timelines and stabilizes rural economies.

🚗 Automotive Tier Networks

Major automakers increasingly offer SCF programs to their upstream suppliers. Parts manufacturers gain faster liquidity via early payments tied to the automaker’s stronger credit rating—mitigating financing costs and enhancing supply chain stability without the OEM holding inventory.

🧊 Retail & Cold Storage

Back to frozen logistics: when a distributor’s inventory is stored in a privately operated cold warehouse, it becomes instantly financeable. More than just a box of fish, it’s a monetizable asset stream that allows structured repayments as inventory is sold—each pallet scanned, shipped, and linked to a financing tranche.

This model marries operational discipline with capital efficiency, and it’s becoming a blueprint for integrated logistics-finance models across other sectors.

The Dark Side: Greensill, Stenn, and the Case for Caution

History has shown what happens when this line is ignored.

🔻 Greensill Capital: From Fintech Darling to Regulatory Warning

Once valued in the billions, Greensill blurred the boundary between SCF and speculative future receivables. With minimal disclosure, it financed deals that hadn’t yet materialized and exaggerated its role in "real economy" finance. The collapse exposed holes in oversight, sparked global investigations, and became a case study in financial alchemy gone awry.

⚠️ Stenn: Another Cautionary Tale

More recently, fintech lender Stenn faced severe allegations around fake invoices and fictitious counterparties. Despite near-unicorn status, its foundation crumbled under scrutiny—echoing many of the red flags that preceded Greensill.

Both cases proved the danger of unlicensed or loosely regulated operations masquerading as finance providers. Without transparency, real collateral, and infrastructure, the façade doesn’t hold.

Pros, Perils, and the Path Forward

✅ The Real Benefits of Proper SCF

- Liquidity Without Balance Sheet Bloat: Suppliers receive early payments, smoothing working capital cycles.

- Lower Cost of Funds: Tied to buyer creditworthiness, not the supplier’s.

- Relationship Capital: Structured finance builds trust and enhances resilience between stakeholders.

- Revenue Diversification: Providers offering bundled services—storage, logistics, and finance—capture multiple value streams while maintaining asset visibility.

❌ Risks and Regulatory Red Flags

- Collateral Quality Risk: Perishable or volatile assets can undermine loan security.

- Opaque Structuring: Without third-party audits and clarity, deals may mask trading as finance.

- Concentration Risk: Relying on a few anchor institutions exposes the chain to systemic shocks.

- Operational Complexity: End-to-end integration of IT, logistics, compliance, and finance is not for the faint of heart.

Regulation, Transparency, and the Call for Separation

If SCF is to evolve from a niche tool into a mainstream capital conduit, it must be ringfenced from the trading masquerade. The path forward demands:

- Strict Separation: Financial services must be structurally and legally distinct from trading desks.

- Institutional Licensing: Only regulated, audited entities should be allowed to facilitate SCF at scale.

- Asset Transparency: Warehouses, storage systems, and inventory records must be verifiable and insurance-backed.

- Auditable Trail: Invoice, contract, and goods flows must be digitally synchronized and independently reviewable.

Infrastructure is the New Collateral

As global trade reconfigures in an age of fragility and AI-driven logistics, trustworthy SCF models are no longer optional—they are mission critical. But trust cannot be built on contracts alone. It must rest on infrastructure—warehouses, silos, delivery networks, and the real-time tracking systems that knit the physical and financial together.

True supply chain finance doesn't speculate. It supports. It facilitates. It unlocks liquidity from ice-cold assets, grain-filled silos, or unglamorous inventory, turning them into financial arteries for the real economy.

The future of trade finance isn't about who can lend the fastest. It’s about who can prove they’re lending with discipline, transparency, and physical custody. That’s not just finance—it’s finance with a backbone.

For high-net-worth investors, institutional allocators, and financial engineers seeking robust yield with real-asset backing, the message is clear: if the operation doesn’t own the infrastructure, it probably doesn’t own the risk either.