In a move that has rattled markets, infuriated retail investors, and revived questions about corporate accountability, former Nikola CEO Trevor Milton has been granted a full pardon by President Donald Trump.

Trevor Milton, founder and former CEO of Nikola Corporation. (bwbx.io)

The timing is striking: Milton’s legal victory arrives just weeks after Nikola Corporation—the once-celebrated hydrogen trucking startup he founded—filed for Chapter 11 bankruptcy protection, capping off one of the most dramatic rise-and-fall stories in clean energy history.

“This is just a signal to everyone that fraud is okay as long as you’re rich,” one commenter wrote online, echoing a sentiment now roiling the investment community. The outrage is not just emotional—it's financial, and it’s structural. The pardon arrives as hydrogen trucking finds itself at a critical crossroads, caught between bold vision and brutal economic reality.

Nikola Corporation (NKLA) Stock Performance Summary

Date

Event

Price (USD)

Note

June 4, 2020

Started trading as NKLA after SPAC merger

~$34 (Opened around $37.55, closed at $33.75)

Merged with VectoIQ Acquisition Corp. (VTIQ)

June 9, 2020

All-Time High (Closing Price)

$93.99 (Adjusted for splits)

Highest closing price recorded

February 19, 2025

Filed for Chapter 11 Bankruptcy

Not provided

Nikola and certain domestic subsidiaries filed for bankruptcy

Milton, once lauded as the Elon Musk of hydrogen, was convicted in October 2022 of securities fraud and wire fraud after misleading investors about the capabilities of Nikola's technology. In December 2023, he was sentenced to four years in prison but had remained free on a $100 million bond while appealing his case.

That legal journey took an extraordinary turn this week.

Did you know that securities fraud is a serious financial crime that can take many forms, all centered around deceiving investors or manipulating financial markets? It typically involves providing false information or omitting crucial facts about securities, with the intent to mislead investors. This can include insider trading, accounting fraud, Ponzi schemes, market manipulation, and more. Securities fraud requires several key elements: a material misrepresentation or omission, intent to deceive (scienter), investor reliance on the false information, and resulting financial losses. Both the SEC and state authorities can pursue civil and criminal charges against those involved in securities fraud, with penalties ranging from fines to imprisonment. The broad reach of securities fraud laws, particularly Rule 10b-5 of the Securities Exchange Act of 1934, aims to protect investors and maintain the integrity of financial markets.

Milton announced on Instagram that President Trump had personally called him to deliver the news of his pardon. “It is no wonder why trust and confidence in the Justice Department has eroded to nothing,” Milton posted, slamming the prosecutors and the judiciary. “I wish judges would stop believing whatever the prosecutors feed them so Americans could trust the justice system again.”

His controversial release now nullifies what prosecutors had hoped would be one of the most consequential white-collar penalties in years. Just two weeks prior to the pardon, federal authorities had sought $680 million in restitution to defrauded Nikola shareholders and another $5 million to a wire fraud victim. Legal experts say the pardon likely cancels those efforts.

A partner at law firm Paul Hastings—where Milton’s brother, Brad Bondi, is a prominent figure—confirmed that Bondi played no role in the pardon process. Still, the optics are combustible, especially given Milton's aggressive political donations. During the 2024 election cycle, Milton poured millions into Republican state parties and campaign committees, raising eyebrows over whether political influence played a role in his absolution.

The White House, where presidential pardons are issued. (wjpitch.com)

Nikola’s rise was meteoric. After merging with a SPAC in 2020, its valuation briefly exceeded that of Ford.

A SPAC, or Special Purpose Acquisition Company, is a shell corporation specifically formed to raise capital through an initial public offering (IPO). The funds raised are then used with the sole purpose of acquiring or merging with an existing private company, effectively taking that company public.

The crescendo came when General Motors agreed to take a $2 billion stake in the company. But that dream unraveled quickly as scrutiny mounted over Milton’s exaggerated claims—most infamously, a demonstration of a truck that appeared to drive under its own power but was later revealed to be rolling downhill.

A Nikola truck appearing to drive, later revealed to be rolling downhill. (redd.it)

By February 19, 2025, Nikola had filed for bankruptcy. It plans to sell off remaining assets via the Delaware bankruptcy court, with a deal expected by mid-April. On March 24, it announced its intention to delist from Nasdaq and deregister from the SEC. A Form 25 is slated for April 3.

For many investors, the loss is not just monetary—it’s existential. “We believed in clean tech, in climate solutions,” said one investor who asked to remain anonymous. “What we got was a lesson in due diligence.”

Hydrogen-powered trucks once seemed poised to revolutionize freight, offering longer ranges and faster refueling than battery electric vehicles (BEVs). But the vision has been undermined by harsh realities: exorbitant production costs, anemic infrastructure, and shaky investor confidence. Analysts now warn that Nikola’s failure—and Milton’s exoneration—could sour sentiment across the entire sector.

A hydrogen refueling station designed for heavy-duty trucks. (squarespace-cdn.com)

“Investors were already hesitant due to the capital-intensive nature of hydrogen. This just piles on the risk perception,” said one clean tech analyst. “The idea that founders can escape financial accountability makes the space look more like the Wild West than a maturing market.”

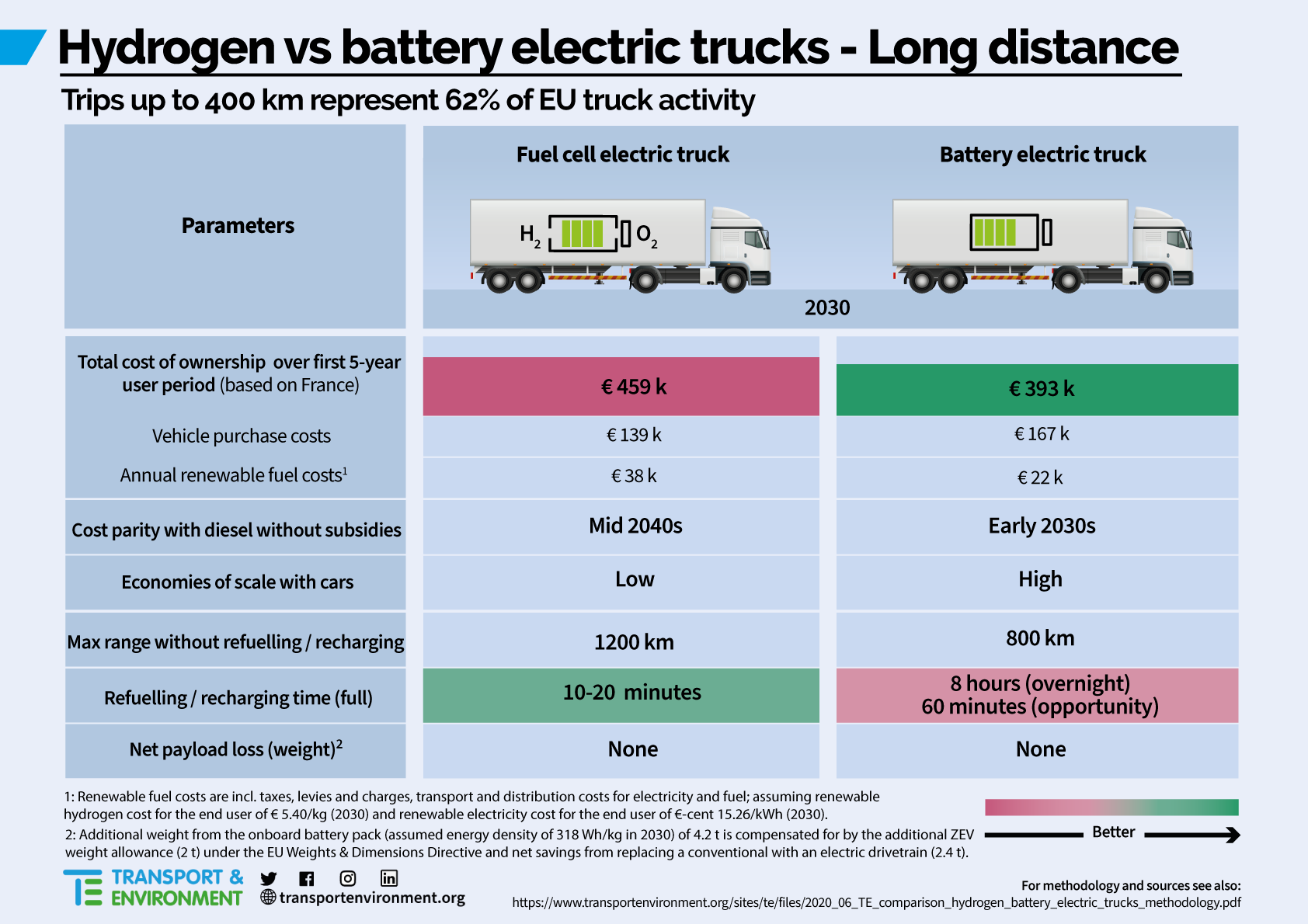

While hydrogen fuel cells offer theoretical advantages, BEVs are closing the gap. Advances in battery range, efficiency, and cost are tilting the equation. Fleet operators, who were once wooed by hydrogen’s fast refueling times, are now leaning toward battery solutions that come with lower maintenance and established infrastructure.

Comparison of hydrogen fuel cell truck and battery electric truck concepts. (transportenvironment.org)

Table: Key Components and Processes in Hydrogen Fuel Cell Trucks

Component/Process

Description

Hydrogen Storage

Pressurized hydrogen gas stored in special tanks

Fuel Cell Stack

Site of electrochemical reaction between hydrogen and oxygen

Electricity Generation

Fuel cell produces electricity to power electric motor(s)

Emissions

Only byproducts are water vapor and heat

Energy Management

Power electronics controller manages electricity flow

Refueling

Similar to conventional trucks, but with pressurized hydrogen

“The hydrogen promise is still alive—but barely,” said an industry observer. “Unless there’s a massive policy push or cost breakthrough, the sector may remain a niche play for the foreseeable future.”

Projected Total Cost of Ownership (TCO) Comparison for Heavy-Duty Trucks by Powertrain Type

Powertrain Type

Projected TCO Parity

Key Cost Factors

Notable Trends

Diesel (ICE)

Baseline

Fuel, maintenance, potential carbon taxes

TCO may increase due to stricter regulations

Battery Electric

2025-2028 (long-haul)

High initial cost, lower energy and maintenance costs

Projected least-cost option by 2030 in Europe

Hydrogen Fuel Cell

2030-2035

High initial cost, expensive fuel, infrastructure costs

May remain 10-20% costlier than battery electric long-term

The biggest losers in Nikola’s collapse may be retail investors, many of whom were drawn in by the green-tech boom and Milton’s charismatic pitch. Now, the prospect of restitution has vanished with the stroke of a presidential pen.

“There’s no justice here,” one investor wrote. “We lost our savings, and he gets a documentary deal.”

Indeed, Milton now plans to tell his version of the Nikola story through a self-produced documentary, a move seen by many as a way to rebrand himself as a misunderstood innovator rather than a convicted fraudster.

Institutional investors are reassessing risk across the clean tech landscape. Some are shifting funds toward more stable battery-electric ventures. Others are demanding ironclad governance before placing bets on the next big idea.

“The market is in a Darwinian phase,” one hedge fund manager said. “Survival won’t be about technology alone. It’ll be about discipline, transparency, and trust.”

The pardon is already reverberating through Washington. Some legislators, especially those with climate-focused constituencies, are calling for tighter oversight of SPACs and green-tech disclosures.

The U.S. Securities and Exchange Commission (SEC) headquarters. (wikimedia.org)

“This is not just about Milton,” said a policy analyst. “It’s about whether the government is enabling or regulating speculative hype.”

Simultaneously, federal and state regulators backing hydrogen infrastructure with public funds may face increased scrutiny. There is a growing chorus urging that any future grants be tied to demonstrable governance and real-world deployment milestones.

Consolidation Ahead: With Nikola’s fall and investor disillusionment rising, expect weaker hydrogen startups to fold or merge. Survivors will likely partner with battery players or legacy manufacturers.

Capital Flight to Batteries: Absent a radical cost drop, capital may continue shifting to BEV platforms. Hydrogen trucking may survive as a niche, especially in long-haul or specialty applications.

Policy-Driven Lifeline: Government incentives may remain the last pillar holding hydrogen afloat. But as scrutiny intensifies, funding may come with stricter strings attached.

Despite the scandal, some see Milton’s pardon as clearing the deck for more credible players. “The bad actors are being flushed out,” said one venture investor. “Now the adults can get to work—if they still have the capital.”

The Trevor Milton saga is not just about one man’s fall and redemption. It’s about the collision between hype and accountability in one of the most capital-intensive corners of clean energy.

The pardon doesn’t erase the damage—it amplifies it.

It tells investors that the rules are optional if you play them right. It tells policymakers that oversight gaps still exist in SPAC-fueled exuberance. And it tells the hydrogen trucking industry that it must now earn back trust, dollar by dollar, and mile by mile.

As hydrogen players regroup and the market recalibrates, one thing is certain: the road to decarbonizing heavy transport just got steeper—and far more treacherous.

You May Also Like

This article is submitted by our user under the News Submission Rules and Guidelines. The cover photo is computer generated art for illustrative purposes only; not indicative of factual content. If you believe this article infringes upon copyright rights, please do not hesitate to report it by sending an email to us. Your vigilance and cooperation are invaluable in helping us maintain a respectful and legally compliant community.

Subscribe to our Newsletter

Get the latest in enterprise business and tech with exclusive peeks at our new offerings

We use cookies on our website to enable certain functions, to provide more relevant information to you and to optimize your experience on our website. Further information can be found in our Privacy Policy and our Terms of Service . Mandatory information can be found in the legal notice